Today, many individuals find themselves trapped under the weight of high-interest debt, struggling to make minimum payments and dreaming of a debt free life. The good news is that with the right strategies and a commitment to personal finance, it’s possible to break free from the shackles of debt and achieve financial freedom. In this comprehensive guide, we will explore various strategies and mindsets required to become debt free as well as using debt as a leverage to create wealth.

By the end of this article, you’ll have a clear understanding of how to become debt free, live a debt-free lifestyle, save more money, and maintain a good credit score. Having a good credit score exposes you to many opportunities, giving you the chance to borrow more and leverage your new borrowed funds into investment opportunities. When you have cleared our debts, the question becomes “now what?”, as someone who has been in your shoes, getting into debt and getting out of debt, I believe it is very important to also learn how to take advantage and use debt as an opportunity to create wealth.

Why is Debt Bad?

Bad debt, as the name suggests, is the less favorable side of borrowing. It can be likened to a ball and chain, a burden that weighs down on your financial progress. The more bad debt you accumulate, the more you become enslaved by it, laboring tirelessly just to keep up with the repayments. In some extreme cases, the stress and anxiety associated with mounting debt can push individuals to the brink, resulting in severe consequences such as suicide. Therefore, mastering the art of handling bad debt is an essential step towards achieving financial freedom.

Assessing your Debt Situation

Understanding your debt is like shining a light on your money situation. It shows you the important numbers, like how much money you owe and how much extra you have to pay because of interest repayments. This helps you make smart decisions about your money.

When you have a lot of debt, it can feel like a huge problem that’s too hard to fix. But looking at your debt helps you see it’s not so scary. You can break it down into smaller parts, like pieces of a puzzle. This makes it easier to see that you can make progress and solve the puzzle over time. As you identify smaller debts within the larger total, you begin to see that progress is not just possible; it’s within your reach. Beyond motivation, this assessment sets the stage for effective financial planning.

How To Assess Your Debt

- Create a Comprehensive Debt List: Start by making a list of all your debts. This includes credit card balances, student loans, car loans, personal loans, and any other outstanding obligations. Don’t forget to include details like the name of the creditor, the outstanding balance, the interest rate, and the due date. The list is in a spreadsheet noting down columns such as due dates, $ amount, Interest Rates for each debt’s minimum payment.

- Gather Statements and Documentation: Collect your most recent statements, loan agreements, and any other relevant documentation for each debt. This will ensure that your assessment is accurate and up-to-date.

- Calculate the Total Debt Amount: Add up the outstanding balances of all your debts to determine your total debt load. This figure serves as a benchmark for your debt repayment journey.

- Minimum Payments: Note the minimum monthly payments for each debt. These are the amounts you are obligated to pay each month to avoid penalties.

- Sum up each payment Minimum Interest + Total Debt Amount: Organize and sum up each of your debt so you know exactly how much debt is being owed and to what it is owed for to tackle our debt.

6 Strategies to get out of Debt

By following this action plan, you can determine how much you can realistically afford to pay on debt, allocate your resources strategically, and work towards becoming debt-free while securing your financial future.

The Debt Snowball and Debt Avalanche – Choose Your Path

When it comes to paying off debt, two popular methods are the debt snowball and debt avalanche. In the debt snowball method, you focus on paying off the smallest debts first while maintaining minimum payments on larger debts. This approach provides psychological motivation as you quickly see small victories.

Alternatively, the debt avalanche method prioritizes paying off debts with the highest interest rates first. While this method may save you more money in the long run, it might take longer to experience the satisfaction of paying off individual debts.

Reduce your Expenses

In today’s consumer-driven world, it’s crucial to assess our spending habits and identify areas where we can cut back. Surprisingly, statistics show that the average American spends approximately $18,000 of their income on non-essential items and services. From dining out frequently to impulse shopping and subscribing to unused memberships, overspending is a common financial pitfall. By taking a closer look at our expenses and making mindful choices, we can significantly reduce waste and allocate those funds towards paying off debt, building savings, and ultimately achieving financial freedom.

A huge pitfall consumers tend to overlook are subscription programs such as Amazon, Netflix, Spotify and more. Monthly payments are commitments we usually overlook. As we dive deeper into our expenses, we should also carefully consider if these monthly payments are worth cutting back based on your current financial situation.

The Role of Personal Loans and Debt Relief

In some cases, personal loans may offer a solution for consolidating high-interest debt, especially if you have good credit. However, it’s essential to weigh the benefits against potential drawbacks, such as origination fees and higher monthly payments.

Debt relief programs are another option for those struggling with unsecured debt. These programs negotiate with creditors to reduce the amount you owe, making it more manageable to pay off your debts.

Debt Consolidation – Simplify Your Finances

Debt consolidation is another approach to streamline your debt repayment journey. This strategy involves taking out a personal loan or opening a credit line to pay off multiple debts at once. By consolidating your debts, you can often secure a lower interest rate and make a single monthly payment, making it easier to manage your finances and accelerate your debt payoff.

Balance Transfer Credit Card

One effective strategy for managing high-interest credit card debt is to consider balance transfer credit cards. These cards often offer introductory periods with low or 0% interest rates on transferred balances. By transferring your existing credit card debt to one of these cards, you can save money on interest and expedite your journey toward a debt-free life. However, it’s crucial to research and choose a card with favorable terms and fees to maximize your benefits.

Creating a Budget for Faster Debt Repayment

To expedite debt repayment, creating a budget is essential. Start by tallying up your monthly income and then list all your expenses, separating them into two categories: essential and non-essential. Essential expenses include rent or mortgage, utilities, groceries, and minimum debt payments. Subtract essential expenses from your income to determine your available funds. Next, scrutinize non-essential spending, identifying areas where you can cut back. By reallocating funds from non-essential to debt repayment, you can accelerate your journey to becoming debt-free.

A budget serves as a financial roadmap, guiding your spending and helping you stay on track. It not only ensures that you allocate enough money to meet your minimum debt payments but also enables you to dedicate extra funds towards debt reduction. By adhering to a well-structured budget, you gain greater control over your finances and increase your capacity to repay debt faster.

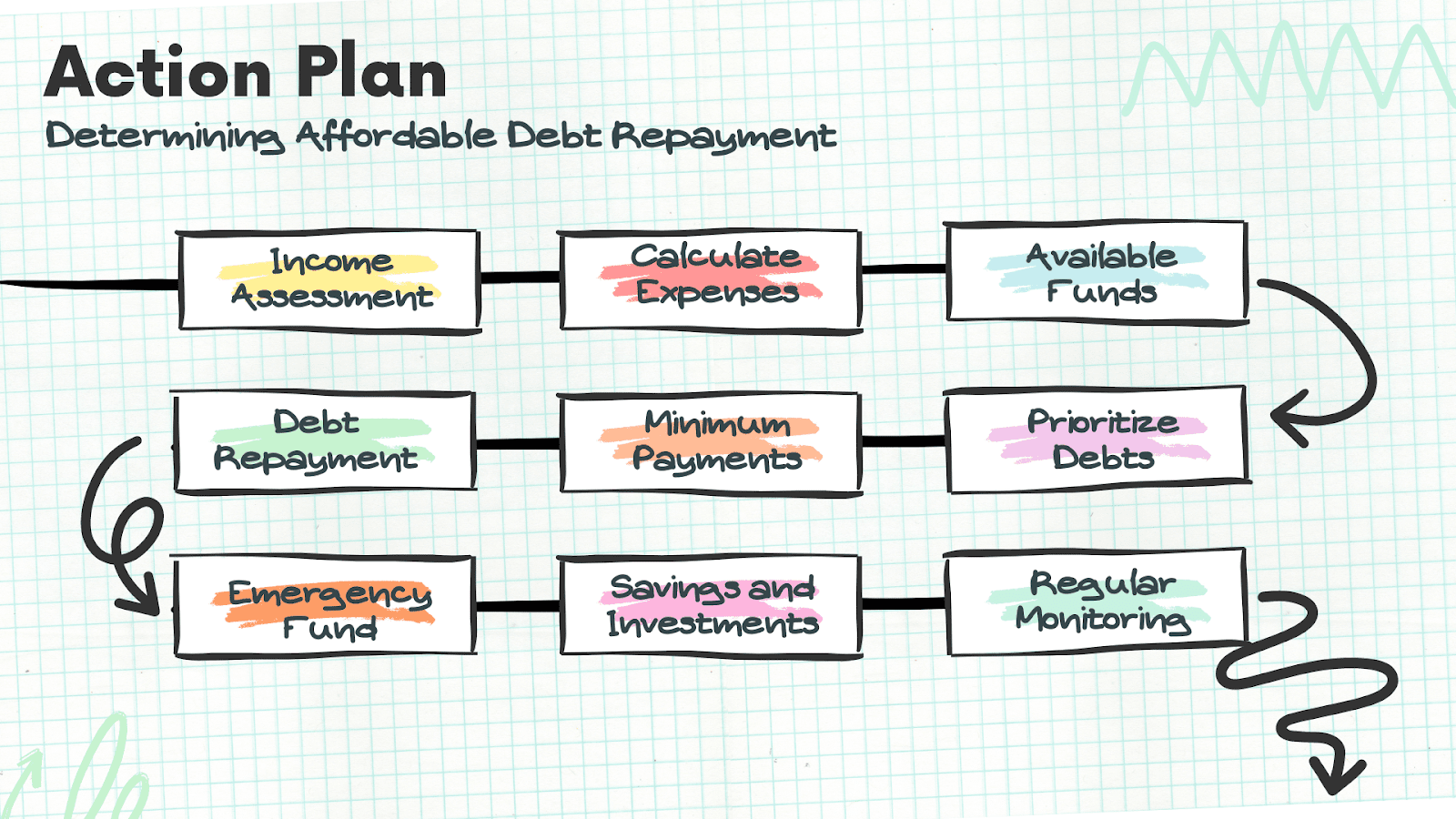

Creating an Action Plan to be debt free: Determining Affordable Debt Repayment

- Income Assessment: Begin by assessing your total monthly income, including your salary and any additional sources of earnings.

- Calculate Essential Expenses: Determine your essential monthly expenses, such as rent or mortgage, utilities, groceries, transportation, and insurance. Subtract these expenses from your monthly income.

- Available Funds: The remaining amount after subtracting essential expenses represents your available funds for debt repayment.

- Prioritize Debts: List all your outstanding debts, including credit cards, loans, and other obligations. Sort them by interest rates, with the highest rates at the top.

- Minimum Payments: Calculate the total minimum payments required for all your debts. Ensure you can meet these minimum payments to avoid penalties and protect your credit score.

- Debt Repayment: Allocate a portion of your available funds to debt repayment, starting with the debt with the highest interest rate. The more you can allocate towards high-interest debts, the faster you can pay them off.

- Emergency Fund: Set aside a portion of your available funds for emergencies to prevent new debt from accumulating during unexpected expenses.

- Savings and Investments: Consider allocating a portion of your remaining available funds toward long-term savings and investments, depending on your financial goals.

- Regular Monitoring: Regularly monitor your progress, make adjustments as needed, and celebrate milestones achieved.

Debt Free Action Plan Example Using The Steps Above

- Income Assessment: Sarah calculates her total monthly income, which includes her $3,500 salary from her full-time job and an additional $500 per month from a part-time gig. Her total monthly income is $4,000.

- Calculate Essential Expenses: She identifies her essential monthly expenses, including $1,200 for rent, $150 for utilities, $300 for groceries, $200 for transportation, and $100 for insurance. Sarah subtracts these expenses from her monthly income: $4,000 – ($1,200 + $150 + $300 + $200 + $100) = $2,050.

- Available Funds: After subtracting her essential expenses, Sarah has $2,050 remaining as her available funds for debt repayment.

- Prioritize Debts: Sarah lists her outstanding debts, starting with credit card debt at a 20% interest rate, a personal loan at 10%, and a student loan at 5%. She prioritizes them by interest rate, with the highest rate first.

- Minimum Payments: She calculates the total minimum payments required for all her debts. Her credit card minimum payment is $75, the personal loan is $100, and the student loan is $50, totaling $225 per month.

- Debt Repayment: Sarah decides to allocate $1,000 from her available funds to debt repayment each month. She begins with her credit card debt since it has the highest interest rate, paying $75 for the minimum payment and $925 extra towards it.

- Emergency Fund: Sarah sets aside $200 per month as an emergency fund to cover unexpected expenses and prevent the need for additional debt.

- Savings and Investments: She allocates $225 per month to a long-term savings account to work towards her financial goals.

- Regular Monitoring: Sarah regularly tracks her debt repayment progress and financial goals, making adjustments as necessary. When she pays off her credit card debt entirely, she celebrates this milestone and redirects the $925 towards her next highest-interest debt, accelerating her path to financial freedom.

Bad Debts to Avoid

High-Interest Credit Card Debt

Credit card debt is one of the most common forms of bad high-interest debt that people struggle with. The allure of buying now and paying later can lead to mounting balances and sky-high interest rates. To begin your journey towards a debt-free life, you must address your credit card debt. Start by assessing exactly how much debt you owe, understanding your monthly payment obligations, and crafting a plan to eliminate this burden.

Payday Loans:

Payday loans are notorious for their high fees and interest rates. An example includes Danny who took out his payday loan when he was 19 years old and ended up with several payday loans costing him $26,000 just under 5 years later.

Predatory Loans

Some installment loans may come with predatory terms that take advantage of high interest rates that could double overnight. Consider Michelle’s story as a warning to stay off predatory loans. Michelle trusted a “friend” who lent her money as part of a predatory loan scheme. The loans started off very small at £50 and very quickly escalated to thousands with threats and death messages sent when repayments are not being made on time.

Unnecessary Consumer Debt:

Suppose you take out a $10,000 loan to finance a luxury vacation, and the loan carries a 10% interest rate. Over time, you could end up paying $2,000 or more in interest, making that vacation significantly more expensive.

Debts without Clear Purpose

Suppose you take out a personal loan for $5,000 but use it for discretionary spending like dining out and shopping. This debt may not enhance your financial situation and could lead to unnecessary interest costs.

Living Debt Free – The Ultimate Goal

The aspiration to live debt-free is a financial dream shared by many. It is the biggest step and pinnacle to begin building real financial freedom, where one’s financial situation is no longer encumbered by the burden of debt. Achieving this goal means being completely debt-free, unshackled from the monthly obligations and interest payments that can erode one’s financial well-being. Beyond the practical benefits, living debt-free also often translates into an excellent credit profile, as managing finances responsibly and eliminating debt are key components of building and maintaining a strong credit history.

Maintaining a good credit score is an essential financial asset that can open doors to numerous opportunities. A solid credit score is a testament to your financial responsibility and can significantly impact various aspects of your life. It allows you to access more favorable interest rates on loans, which, in turn, can save you substantial amounts of money. With good credit, you can leverage debt wisely, such as taking out a mortgage for a home or a loan for an investment, and make your money work for you. “Good debt” in the form of mortgages or business loans, when managed wisely, can enable you to acquire appreciating assets or invest in ventures that yield returns exceeding the cost of borrowing.

““Good debt” makes you money even while having debt, while bad debt takes money from you”.

Having a strong credit history can also lead to lower insurance premiums, better rental opportunities, and even increased job prospects, as some employers may check an applicant’s credit as part of their hiring process. In essence, good credit empowers you to harness financial leverage, improving your financial well-being and expanding your opportunities.

Living debt-free is about more than just eliminating debts; it’s a mindset and a lifestyle; a key step towards living with financial freedom. It means adopting responsible financial habits, avoiding unnecessary debt, and embracing a future where you have the freedom to allocate your income towards your goals and dreams rather than servicing past financial commitments. This lifestyle shift empowers individuals to save, invest, and enjoy financial security, leading to a brighter and more prosperous future. It’s not merely a destination but an ongoing journey towards financial independence and peace of mind.